Previous rules

Patent box relief enables companies to claim an effective 10% rate on patent/IP related profits as opposed to 19% based on current corporate tax rates.

Under the previous patent regime, companies which own a UK or European patent (or exclusive rights to that patent), which elected into the patent box on or before 30 June 2016 could use the old regime when calculating their IP profits as part of the transitional rules. However, from 1 July 2021, the transitional rules will cease and companies will be required to use the new regime when calculating their IP profits.

New Regime

Under the new rules, the changes are as follows:

- Mandatory streaming is now required – The new rules mean that existing (and new) claimants will be expected to allocate IP income and expenditure to a separate stream for each specific IP asset.

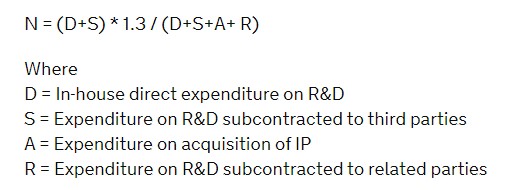

- Introduction of the so called R&D fraction – which was introduced to ensure that the benefits only apply to companies who undertake substantial R&D activity. This new step in the calculation restricts the overall benefit based on the level of R&D costs incurred by the company against the total costs of creating the IP asset, including, the acquisition of IP rights or work from related party subcontractors. This also requires companies to hold retailed records dating back to 1 July 2016 at a minimum, but it is possible to look as far back as 20 years before the last day of the relevant accounting period if this gives a more favourable result. (This is also known as ‘tracking and tracing’.

- You will need to consider how you will stream the costs as this determines how you split out the R&D costs,

The nexus fraction is calculated as follows:

This means that if the development expenditure is incurred by a group company, before the IP is transferred, the level of Patent Box relief available will decrease. However, in this case restructuring should be considered in advance to see if the company could achieve a better result.

Do I need to track and trace if my company has undertaken all development expenditure in-house and there are no acquisition costs?

The company can use this evidence instead of tracking actual R&D costs and HMRC considers this acceptable.

However, consideration must be given to future activities, for example how the acquisition of a qualifying IP right which is incorporated into the same product stream could impact the R&D fraction if your R&D cost history is incomplete.

My company is small, with small amounts of IP income – do I still need to stream under the new rules?

The company may be able to elect for global streaming treatment, whereby all IP income is included in one stream.

The legislation requires the qualifying company to make this election in the first year of using the new rules for it to apply in a subsequent period, even if it is not required in the earlier year. In effect, a protective election is required.

However the company should continue to track and trace expenditure again, in case future plans such as the purchase of IP into a stream or the company becomes too large for Small Claims Treatment (currently where the residual IP profit of the trade for an accounting period exceeds £1m, or £3m collectively where part of a group).

My company doesn’t meet the criteria for Small Claims Treatment/Global Streaming Treatment, how do I track and trace expenditure? How do I stream expenditure?

Streaming should be done on a just and reasonable basis, for example, per patent, or per product group or process.

The extent of records required to ensure accurate tracking and tracing of R&D expenditure will vary between companies depending upon the extent of the R&D they undertake and the amount of IP that they own. Companies making R&D tax credit claims are likely to be familiar with extracting R&D expenditure and this can be used as a starting point. Companies should also demonstrate and include details of the methodology by which R&D expenditure is allocated to individual sub-streams, at least in the first such period of calculation, and detail any significant adjustments to their methodology arising in subsequent years.

For further information please contact either Anthony Lalsing or Donna Kenyon via their profiles below:

Contact Our Experts