There’s a lot to do when expanding business operations into a new global market, and given the new opportunities that are on offer, it’s tempting to just get on with it. However this is one time when it definitely makes sense to pause for thought, as the way in which the market is approached will undoubtedly have consequences further down the line.

Getting the right structure in place from the off, and having a well devised plan of action, can make or break the success of the venture. The typical areas that a business needs to get upfront visibility on include:

- Group structure and local entities;

- Financing the operations and cash management;

- Trading arrangements and profit positioning;

- Tax, accounting and legal issues.

Bringing this all together in a coordinated fashion will provide the framework that a well-run business needs if it is going to be on the front foot with its expansion plans. Of course, there is a lot to be done, but it will feel good that you are taking control of the process and not just reacting to the multitude of questions and issues that will arise.

The remainder of this article will focus on just one of the early stage issues that needs to be resolved; the corporate structure and the use of a holding company to better support the international business expansion.

Reasons and uses of a holding company structure

When a business expands into a new market, an early discussion will be around the type of local entity to set up, and whether it makes sense to establish a branch or a subsidiary company. Some of the factors to consider are shown in the table below:

Branch

- Use of overseas tax losses

- No shareholding considerations

- Limit associated companies

- Easier to wind up

- Can be incorporated if appropriate

- Exemption system available

Subsidiary

- More substantial presence

- Commercial liability ring-fenced

- Tax exposure ring-fenced

- Easier profit determination

- Access local tax advantages

- Tax efficient exit

- Management and control issues

The choice between using a branch or subsidiary cannot just be answered from a home country perspective, and local advice will be required to understand the implications in the market that you are targeting. It will also be necessary to determine how the local entity will be classified from a UK perspective as this will affect the structuring arrangements.

If the decision is made to set up a subsidiary company, one of the questions that will need to be considered is ‘who will own the shares in this company?’ In this respect, just using an existing trading company can lead to the following concerns:

Risk: having the subsidiary as an investment of an active trading company increases the commercial risk of the group;

Governance: the parent company has conflicting roles, acting as both an investment and trading company;

Strategic: the structure doesn’t cater well for expansion or exit, and a future reorganisation could be expensive.

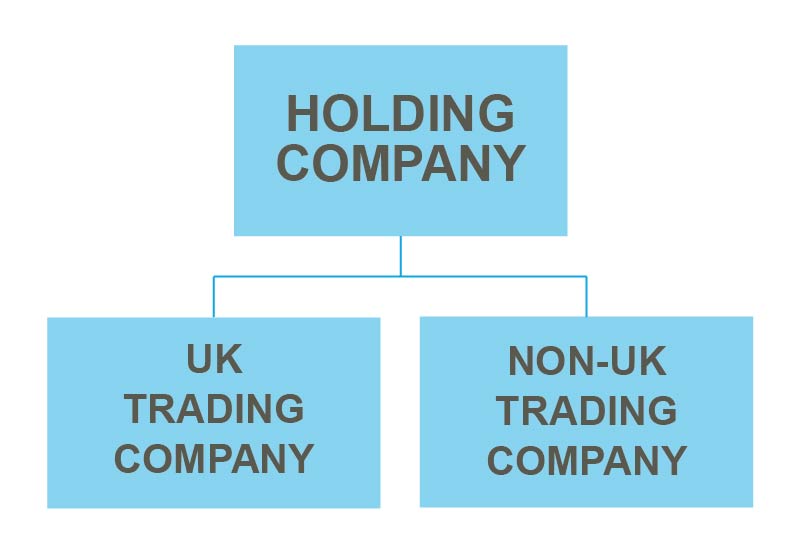

It can often be preferable to remove these concerns, especially if you may be looking to set up in other locations, and to instead adopt a holding company structure. This will typically have a passive company established as the parent of a group, with the trading entities then being held directly by the parent company as follows:

Although the holding company is a non-trading company, it does still have an active role to play in managing the group, including:

- Strategic management: providing direction and oversight of the group activities and financial performance;

- Cash management: including repatriation from, and provision of finance to, the subsidiaries;

- Profit management: the holding company can hold the Intellectual Property and undertake the centralised functions for the group;

- Reporting: current and future subsidiaries are consolidated under one holding company, improving the visibility of the financial results for management and group reporting purposes.

The advantages that a holding company brings to the corporate structure means that it is often beneficial to go through a restructuring process before setting up a new entity in the target market.

Establishing a holding company

To establish a new holding company for a group, the shareholders in an existing trading company (“TradeCo”) would dispose of their shares in TradeCo and in exchange receive shares in a new holding company (“Holdco”).

Share exchange transactions can often be undertaken by UK resident shareholders on a tax neutral basis. However, advance tax clearances should be obtained from HM Revenue and Customs to ensure that the transfer of the shares in TradeCo to Holdco does not give rise to Capital Gains Tax, Income Tax or Stamp Duty in the UK.

The resulting structure can then be used to support the international expansion as the shares in UK and non-UK trading companies are held directly by the new holding company.

Features of a holding company

In terms of the features of a holding company, there are many factors, tax and non-tax, that should be taken into account when assessing where to locate the holding company. A holding company should be considered in relation to commercial implications as well as the desirable features from a tax perspective. These can be summarised as follows:

Commercial

- Geographical location and accessibility for shareholders and directors

- Stability and robustness of the legal systems

- Cost and governance requirements

Taxation

- Acceptability – acceptable to the shareholders tax authorities

- Treaty network – a wide and well established treaty network

- Inbound dividends – exemption from tax on dividends received

- Withholding taxes – minimal withholding tax on dividends, interest and royalties paid

- Anti-avoidance legislation – minimal anti-avoidance legislation

- Corporate tax rates – low corporate tax rates

- Capital or stamp duties – minimal capital or stamp duties on share transactions

- Treatment of capital gains – exemption from tax on disposal of subsidiaries

- EU Directives – access to EU Directives

The importance and relevance of each factor varies depending on the exact corporate and shareholder circumstances. For SME companies, it is not usually appropriate to establish a non-UK holding company where the main shareholders are UK domiciled and resident individuals. This is because true management and control of the group is most likely to come from the UK, and there are not usually sufficiently compelling commercial reasons why a non-UK holding company would be necessary.

Taxation

It is also fair to note that the UK has a well-established and attractive tax regime for holding companies. There are elements of the regime that are complex, such as the dividend and capital gains exemptions, as well as the anti-avoidance legislation, but all the main attributes of an internationally competitive holding company regime are in place to mean that the UK will be a holding company location of choice for groups trading on an international basis. The holding company regime is briefly summarised below:

| HOLDING COMPANY REGIME | UK |

| Corporate tax rate | 19% |

| Double Tax treaties | Excellent extensive network (in excess 130 countries) |

| Dividend repatriation to UK | Taxable, but exemption may be available |

| Anti-avoidance rules | Controlled Foreign Company regime |

| Disposal of subsidiaries | Taxable, but exemption may be available |

| Withholding tax on dividends paid | None |

| Pre-transaction rulings | Available on significant commercial transactions |

| EU Directives | Pre-Brexit access to EU Directives |

In relation to a future exit and sale of the shares in the holding company, it should be appreciated that UK tax rules generally focus on the tax residence of the shareholder rather than the location of the company. Establishing a holding company in an offshore jurisdiction does not reduce the level of UK capital gains tax payable on the sale of a company by a UK resident and domiciled shareholder.

Step by step

Taking care to determine the most appropriate corporate structure should form part of the early stage decision making when planning for international expansion. It is only once the structure has been agreed that it will be possible to resolve some of the other fundamental structuring issues that relate to the cross-border finance and trading arrangements.

Contact Our Experts